2026 MBS Stress Test: Fed Capital Rules and Mortgage Rates

The 2026 MBS Stress Test: Regulatory Relief and the U.S. Mortgage Landscape

The Federal Reserve’s finalized 2026 severely adverse scenarios have implicitly introduced a wave of regulatory relief that could fundamentally reshape the U.S. mortgage landscape. The central bank recently finalized its 2026 hypothetical testing parameters for 32 large banks, executing a critical policy maneuver by freezing current stress capital buffer (SCB) requirements until 2027 to incorporate public feedback, according to the Federal Reserve Board.

By intentionally pausing new capital hikes and introducing targeted revisions to the global market shock component, regulators are signaling a more measured, accommodative approach to bank capital frameworks. For the domestic housing market, this regulatory stabilization matters immensely. It establishes a highly anticipated MBS Stress Test dynamic that incentivizes large financial institutions to step back into the agency mortgage-backed securities (MBS) market. This institutional pivot has the potential to drive down consumer mortgage rates, offering a critical release valve for homebuyers even if baseline Treasury yields remain stubbornly elevated.

To understand the profound implications of this regulatory event, market participants must look beyond the headline macroeconomic shocks and examine the mechanical adjustments made to the test’s trading parameters. The Federal Reserve’s decision to maintain existing capital buffers rather than immediately tightening them blunts the immediate punitive impact of the severe real estate shocks modeled in the 2026 framework.

This is not merely a bureaucratic delay; it is a highly actionable signal that alters the risk-reward calculus for bank treasury departments. By normalizing the shock assumptions for government-backed assets, the Fed effectively lowers the hurdle rate for banks to hold them. This makes agency MBS a substantially more attractive yield play relative to the regulatory capital required to carry them on institutional balance sheets.

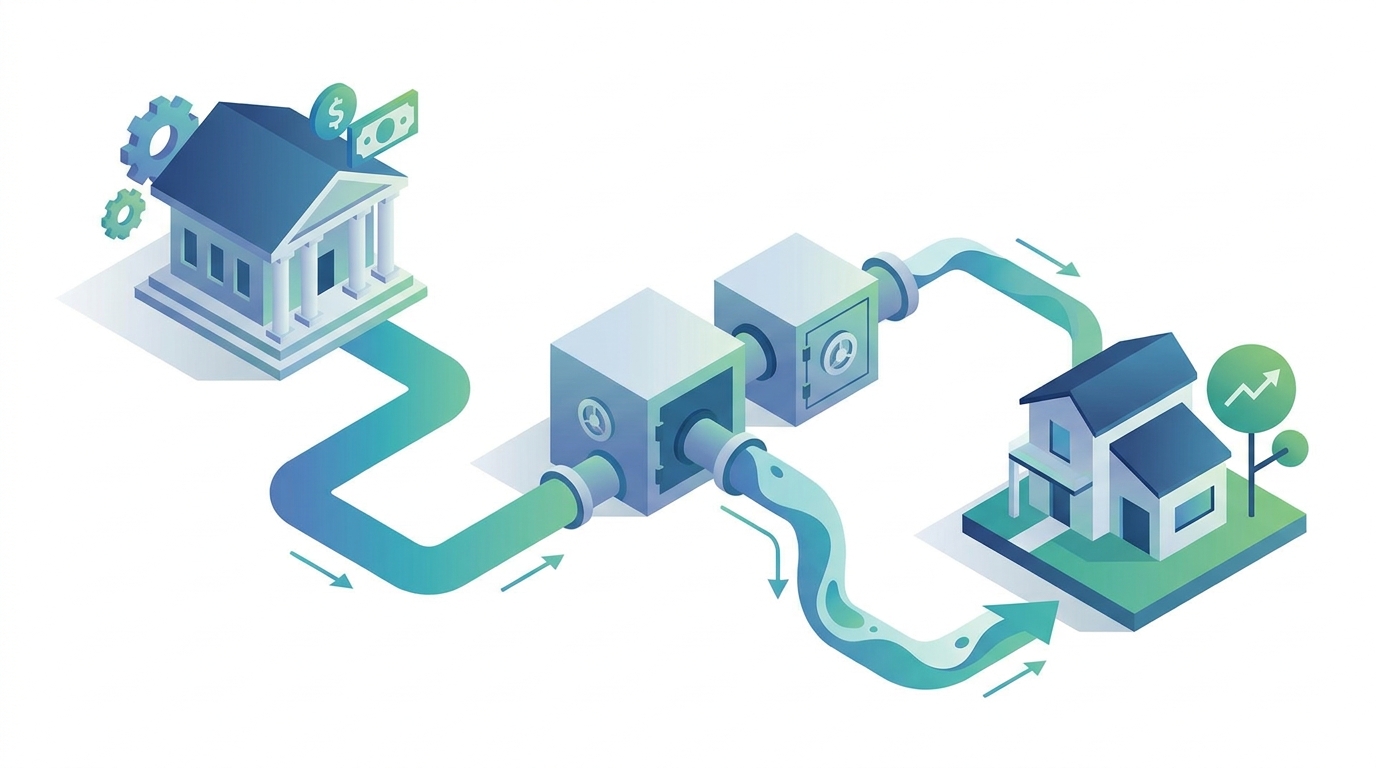

The Transmission Chain: From Regulatory Tweak to Main Street Rates

To understand how a highly technical regulatory tweak in Washington alters borrowing costs on Main Street, investors must map the stress test transmission chain. Previously, the proposed 2025 Scenario Design Policy Statement added strict guides for calibrating variables such as mortgage spreads. The proposed 2026 scenario deliberately pushed the mortgage rate spread toward the more severe half of its possible range, according to BPI.

If the Fed’s final revisions to the global market shock component temper these severe MBS shock magnitudes for trading desks, it creates a powerful, albeit implicit, capital relief mechanism. When hypothetical stress scenarios assume less catastrophic widening in mortgage spreads, banks are ultimately required to hold less protective capital against their agency MBS portfolios.

This dynamic transforms a highly punitive regulatory environment into a more neutral, functioning one. Mapping this exact transmission mechanism reveals how institutional regulatory policy dictates consumer borrowing costs at the retail level.

The sequential path demonstrates how adjusted stress test parameters theoretically cascade through the broader financial system. The table below outlines this progression from the initial regulatory event down to the final impact on the domestic housing market. By tracking these four distinct steps, investors can pinpoint exactly where institutional capital relief translates into tangible market liquidity.

| Phase | Transmission Step | Market Mechanism & Effect |

|---|---|---|

| 1. Event | Fed finalizes 2026 scenarios | Revisions to the global market shock component aim to improve consistency and plausibility for trading exposures. |

| 2. Mechanism | Lower hypothetical capital penalties | 32 large banks face less severe modeled losses on agency MBS, reducing the capital they must hold against these assets. |

| 3. Market Effect | Increased bank demand for MBS | With lower capital constraints, banks re-enter the market as active buyers, improving overall MBS liquidity. |

| 4. End-User Impact | Spread compression & lower rates | The primary-secondary mortgage spread compresses, allowing originators to offer homebuyers lower mortgage rates. |

The second-order effects of this transmission chain are highly consequential for fixed-income markets. Large U.S. banks have historically served as the primary liquidity providers for the agency MBS market. However, punitive capital rules over the past few years have forced them to pull back, widening spreads and increasing market volatility.

By improving the plausibility of the global market shock, the Federal Reserve implicitly reduces the friction for these 32 large banks to warehouse mortgage risk, as noted by the Federal Reserve Board. Increased bank participation absorbs excess supply in the secondary market, which stabilizes MBS valuations and lowers the yield required by institutional investors.

For market participants, this signals that agency MBS could see structurally supported demand from domestic depositories. This renewed institutional sponsorship serves to counteract some of the prevailing headwinds generated by the central bank’s ongoing quantitative tightening program. Ultimately, the success of this transmission chain culminates in the primary-secondary mortgage spreadthe critical gap between what homebuyers pay and what MBS investors yield. When banks bid up MBS prices, secondary yields fall, granting mortgage originators the margin necessary to lower primary rates for consumers without sacrificing profitability.

Highest-Signal Evidence: Severe Baselines vs. Capital Reprieves

The Federal Reserve’s finalized 2026 severely adverse scenario establishes a rigorous baseline for evaluating the resilience of the banking sector against a severe global recession. Providing clear, chart-friendly numeric context, the framework simulates a catastrophic macroeconomic contraction characterized by a 5.5 percentage point surge in the U.S. unemployment rate, peaking at 10 percent.

Alongside this severe labor market deterioration, the Federal Reserve models a devastating 30 percent plummet in residential house prices and a steep 39 percent decline in commercial real estate (CRE) valuations. By imposing these extreme parameters, regulators are forcing institutions to demonstrate solvency under conditions that mirror the absolute worst historical downturns. For U.S. investors, this provides the highest-signal evidence that the central bank remains deeply concerned about the latent vulnerabilities embedded in consumer credit and commercial property markets.

The sheer magnitude of the modeled real estate collapse serves as a critical indicator of regulatory anxiety regarding asset deflation. A 39 percent decline in CRE prices and a 30 percent drop in residential housing would effectively wipe out the equity buffers on highly leveraged property loans across the entire financial system.

The National Credit Union Administration has also aligned its 2026 supervisory stress test scenarios with the Fed’s domestic parameters, ensuring that credit unions face the exact same stringent evaluation. This unified regulatory posture implies that both banks and credit unions will likely preemptively tighten their underwriting standards and increase loan loss reserves to prepare for potential balance sheet stress. Consequently, market participants should anticipate constrained credit availability in the real estate sector, potentially accelerating the very price corrections the models are designed to simulate.

Beyond traditional lending books, the 2026 scenario also introduces targeted adjustments for institutions with significant capital markets exposure. The Federal Reserve implemented two specific revisions to the global market shock component applied to banks with large trading operations. Regulators stated these changes are designed to improve consistency across shocks applied to similar exposures and enhance overall plausibility.

While the exact technical details of these revisions remain somewhat opaque in the public release, the analytical implication is clear. Regulators are actively refining their tools to capture complex counterparty risks and liquidity mismatches that previous stress tests may have missed. Investors holding equity in major money-center banks must monitor trading revenues closely, as these refined shocks may force institutions to hold higher capital against specific derivative or trading book exposures in the future.

Despite the draconian severity of the testing parameters, regulators have offered large banks a significant near-term reprieve regarding their actual capital requirements. The Fed board voted to maintain the current stress capital buffer (SCB) requirements until 2027, deliberately delaying the implementation of new requirements to allow time to calculate them using models that incorporate public feedback. As noted by the ABA Banking Journal, this pause is intended to correct any deficiencies in the supervisory models before binding capital constraints are applied.

For the market, this verified regulatory delay is a highly actionable signal. It provides the 32 tested banks with a full year of capital planning certainty. Without the immediate threat of abruptly higher SCB minimums, these institutions can more confidently execute their existing shareholder return programs, including planned stock buybacks and dividend distributions throughout 2026.

However, market participants must strictly separate the verified facts of this regulatory delay from the speculative market inferences it has generated. While the postponement of new SCB requirements to 2027 is a confirmed policy decision, the projected scale of a resulting MBS buying spree remains unverified market conjecture. Because the finalized rules lack explicit 2025 policy guides for calibrating mortgage spreads or concrete data on future bank asset allocation, the actual scale of any MBS accumulation is highly uncertain.

Scenario Analysis: Base Case, Upside, and Downside Risks

The Federal Reserve’s recent decision to freeze current stress capital buffer requirements until 2027 creates a critical, albeit temporary, window of regulatory stability. By delaying new capital requirements to incorporate public feedback into supervisory models, the Fed has inadvertently established a baseline environment for bank balance sheet strategies over the next year, according to the Federal Reserve. Analyzing how banks will utilize this window requires modeling distinct scenarios based on the finalized evidence.

The Base Case: Measured Accumulation and Modest Relief In our base case scenario, this regulatory pause encourages a measured, calculated return to MBS accumulation by large financial institutions. As banks deploy capital with a clearer near-term horizon, we expect moderate compression in the primary-secondary mortgage spread. For U.S. investors and prospective homebuyers, this translates to slight mortgage rate relief. This dynamic acts as a modest but vital tailwind for a housing market that has been severely constrained by affordability challenges and locked-up inventory over the past several years. Banks will likely use this period to optimize their yield profiles without taking on excessive duration risk, balancing the pursuit of returns with the looming reality of the 2027 model updates.

The Downside Scenario: Defensive Capital Hoarding A distinct downside scenario emerges when analyzing the sheer severity of the Fed’s finalized 2026 stress tests. The “severely adverse” scenario mandates that 32 large banks model an extreme global recession, featuring a 5.5 percentage point surge in the U.S. unemployment rate to a 10 percent peak, per the Federal Reserve. Crucially, this modeled downturn includes a devastating 30 percent decline in house prices and a 39 percent collapse in commercial real estate (CRE) valuations, as detailed by the Federal Reserve.

Faced with these draconian hypothetical shocks, bank risk committees may choose to defensively hoard capital rather than deploy it into MBS. If institutions prioritize liquidity buffers over yield generation to ensure they pass the 2026 evaluations with flying colors, any anticipated MBS demand could evaporate. This would leave mortgage spreads wide, completely negating potential rate relief for consumers.

This defensive posture is further justified by the stringent variable calibrations introduced in recent Fed policy. The proposed 2025 Scenario Design Policy Statement explicitly added guides for calibrating variables such as mortgage spreads and the BBB corporate spread, according to BPI. In the proposed 2026 framework, values for the mortgage rate spread, CRE prices, and the VIX were deliberately pushed toward the “more severe half of their possible range,” noted BPI. By forcing banks to stress-test against heavily widened mortgage spreads, regulators are inherently penalizing heavy MBS concentrations in adverse scenarios. Consequently, second-order effects could see banks structurally reduce their MBS footprint to optimize their stress-test performance, inadvertently keeping borrowing costs elevated.

The Upside Scenario: Aggressive Buying and Market Decoupling Conversely, a powerful upside scenario exists where banks aggressively step in as MBS buyers, fundamentally shifting housing dynamics. If bank treasurers determine that current MBS valuations offer a compelling risk-adjusted premiumespecially compared to the severely stressed BBB corporate spreads modeled by the Fedthey may rapidly accumulate these assets. This aggressive institutional buying would compress mortgage spreads significantly, potentially driving retail mortgage rates down even if benchmark Treasury yields remain high.

For the U.S. housing market, this decoupling of mortgage rates from sovereign Treasuries could serve as the ultimate catalyst needed to unfreeze locked-up housing inventory. Homeowners currently trapped by the “golden handcuffs” of low existing rates might finally find the financial justification to sell, injecting much-needed supply into the market and normalizing transaction volumes.

The Uncertainty Factor Despite these defined scenarios, the ultimate direction of bank balance sheet strategies remains highly uncertain. It is not entirely clear if the finalized 2026 severely adverse scenario retained the unprecedentedly steep yield curvemeasured by the spread between 10-year and three-month Treasuriesthat was featured in the initial proposal by BPI.

Furthermore, while the Fed implemented two specific revisions to the global market shock component applied to banks with large trading operations to enhance consistency and plausibility, according to the Federal Reserve, the technical details remain opaque. Without granular visibility into how these specific shock revisions alter internal bank capital models, analysts must remain cautious about predicting exact MBS purchasing volumes.

What to Watch Next: Leading Indicators for Market Liquidity

The Federal Reserve’s recent decision to maintain current stress capital buffer (SCB) requirements until 2027 establishes a critical transitional window for U.S. financial markets. By pausing updates to allow time for public feedback on supervisory models, regulators have temporarily stabilized capital mandates for the 32 large banks undergoing the 2026 stress tests, according to the Federal Reserve Board. However, because the finalized 2026 severely adverse scenario introduces extreme economic baseline assumptions, investors must assume that banks will use the current cycle to proactively restructure their balance sheets before the revised 2027 models take effect. Consequently, market participants must closely monitor specific leading indicators to gauge how these preparations will impact broader market liquidity.

1. Bank Earnings Calls and Forward Guidance The most immediate indicator to track will be large bank earnings calls, specifically management’s forward guidance regarding mortgage-backed securities (MBS) portfolio allocations. Because the 2026 stress scenario models a severe housing downturn, banks may anticipate that the forthcoming 2027 SCB framework will penalize heavy real estate exposure more aggressively.

If major financial institutions signal a preemptive reduction in their MBS holdings during upcoming quarterly reports, it would directly threaten the efficacy of the MBS liquidity transmission chain. A structural stepback by these traditional anchor buyers would likely force yields higher to attract alternative capital to the market. Therefore, analysts must parse earnings commentary for any explicit shifts in duration risk appetite or agency versus non-agency MBS weighting.

2. The Primary-Secondary Mortgage Spread Index Beyond earnings guidance, real-time tracking of the primary-secondary mortgage spread index will serve as a definitive barometer for the health of the mortgage market. This spread measures the difference between the interest rates charged to retail homebuyers and the yields demanded by secondary market MBS investors.

If large banks begin to retreat from MBS absorption in preparation for the 2027 capital buffer updates, the resulting drop in institutional demand will cause this spread to widen. A sustained widening of the primary-secondary spread indicates a friction-filled liquidity transmission chain, meaning that any future Federal Reserve rate cuts might not effectively pass through to consumer mortgage rates. Monitoring this index provides a quantifiable, high-frequency measure of how regulatory anticipation is altering actual market mechanics.

3. Federal Reserve Commentary and Public Feedback Integration Federal Reserve commentary leading up to the 2027 SCB implementation will also require intense scrutiny, particularly regarding the integration of public feedback. The ABA Banking Journal notes that the Fed board explicitly delayed the new requirements to calculate updates based on models that incorporate this external input.

However, the exact nature of the public feedback that will be used to correct deficiencies in the supervisory models remains highly uncertain at this stage. Investors should watch speeches by Fed Governors and regulatory chiefs for hints on whether the feedback leans toward softening or hardening capital requirements for specific asset classes. Any hawkish regulatory rhetoric regarding real estate exposures could accelerate bank deleveraging, compounding liquidity constraints in the secondary markets.

4. Refinements to the Global Market Shock Component Finally, market participants must track how the Fed refines its global market shock component for banks with significant trading operations. The finalized 2026 scenarios already include two revisions to this component aimed at improving consistency and plausibility, alongside a modeled 39 percent decline in commercial real estate prices, as detailed by the Federal Reserve Board.

Because the specific mechanics of these two revisions remain somewhat opaque, their second-order effects on trading desk behavior are not yet fully understood. If these revisions ultimately translate into significantly higher capital charges for holding trading inventory in 2027, large banks will likely reduce their market-making activities in real estate-linked assets. This would shift the burden of liquidity provision onto non-bank financial institutions, fundamentally altering the risk profile of the U.S. mortgage finance system.

Conclusion

The finalization of the 2026 severely adverse scenarios reveals a Federal Reserve attempting to balance rigorous systemic oversight with necessary market pragmatism. By modeling catastrophic economic conditionsincluding a 10 percent unemployment peak and a 39 percent collapse in commercial real estateregulators are maintaining a highly defensive posture regarding asset deflation. Yet, by deliberately freezing the stress capital buffer until 2027 and implementing plausibility revisions to the global market shock component, the Fed has provided a vital operational runway for the nation’s largest financial institutions.

This nuanced regulatory environment establishes a critical MBS Stress Test dynamic. The evidence suggests that while the baseline macroeconomic models are draconian, the immediate capital reality is accommodative. This implicit relief lowers the hurdle rate for banks to hold agency MBS, paving the way for institutional capital to re-enter the secondary mortgage market.

For the U.S. consumer, this institutional transmission chain is the ultimate mechanism for borrowing relief. If banks utilize this 2026 regulatory window to aggressively capture MBS yield, the resulting spread compression could successfully detach retail mortgage rates from elevated Treasury yields. However, because this relief is explicitly temporary and contingent upon opaque future model revisions, market participants must treat this environment as a fragile window of opportunity rather than a permanent structural guarantee.

Disclaimer: This analysis is for informational purposes only and does not constitute investment, financial, real estate, or legal advice. Always consult a licensed financial advisor before making investment decisions.

FAQ

How does the primary-secondary mortgage spread affect my mortgage rate? The primary-secondary mortgage spread is the gap between the interest rate homebuyers pay (primary) and the yield demanded by institutional investors holding mortgage-backed securities (secondary). When bank demand for MBS increases, secondary yields fall, which compresses the spread and allows mortgage originators to offer lower retail mortgage rates to consumers.

Why did the Federal Reserve delay new Stress Capital Buffer (SCB) requirements until 2027? The Federal Reserve explicitly voted to maintain current SCB requirements until 2027 to allow time to calculate new requirements using supervisory models that incorporate public feedback, effectively correcting deficiencies in their current models before applying binding capital constraints.

Which banks are subject to the 2026 severely adverse stress test scenarios? The Federal Reserve’s 2026 hypothetical stress test scenarios evaluate 32 large banks against a severe global recession.

How do agency MBS shock magnitudes change bank lending behavior? When stress test scenarios assume less severe shock magnitudes for agency MBS, banks are required to hold less protective capital against these assets. This lower capital penalty makes holding MBS more attractive, encouraging banks to re-enter the market as active buyers, which improves overall market liquidity and supports lower consumer borrowing costs.