How the Fed Rate Hold Creates a Real Estate Market Divide

The Great Bifurcation: How the Fed Rate Hold and Structural Capital Costs are Impacting the Real Estate Market

The Federal Reserve’s recent decision to institute a Fed Rate Hold alters the real estate landscape. It shifts a temporary liquidity squeeze into a structural cost-of-capital adjustment. By keeping borrowing costs elevated and signaling a pause in easing, the central bank has highlighted a divergence in the real estate market characterized by two opposing forces.

On the residential side, high rates solidify the “lock-in effect.” Homeowners retain low fixed-rate mortgages, constraining housing supply and slowing transaction velocity. Conversely, the commercial real estate (CRE) sector faces a significant transition as a wave of short-term debt matures through 2026 into a higher-rate refinancing environment.

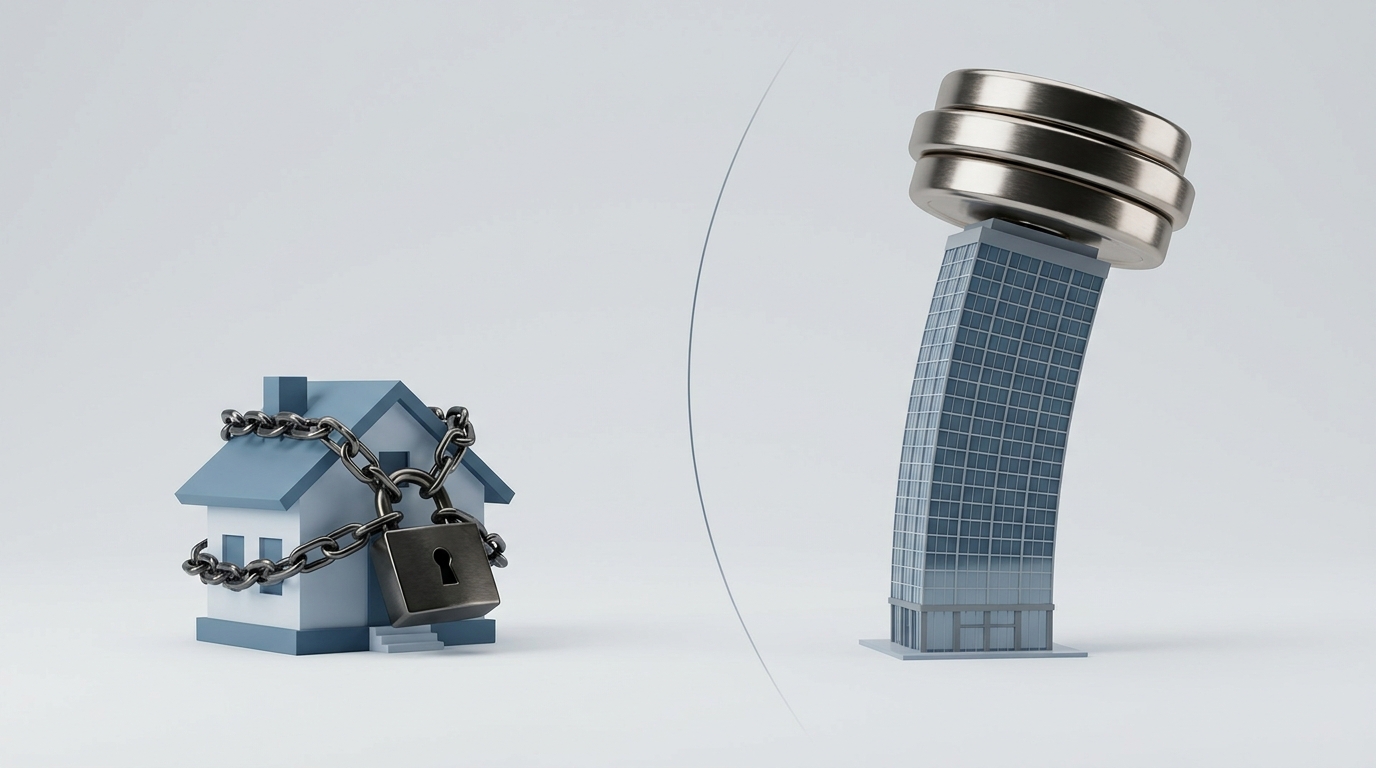

[Graphic Instruction: Insert a dual-axis visual or infographic illustrating the “Real Estate Divergence.” The left side should show a constricted funnel representing the residential lock-in effect with low supply and frozen inventory. The right side should depict a bar chart of commercial debt maturities aligning with higher interest rates.]

This visual captures the structural imbalance defining the current market. Residential real estate is defined by a lack of available assets, supporting prices despite affordability challenges.

In contrast, commercial real estate is characterized by elevated debt levels on depreciating assets. This prompts owners to either inject fresh equity or transfer properties to lenders. For market participants, understanding this bifurcation is foundational for navigating the market over the coming decade.

The Transmission Chain of Monetary Policy

The transmission mechanism of monetary policy into the real estate sector operates with a distinct lag. When the Federal Reserve holds interest rates at elevated levels for prolonged periods, the cost of capital alters market behavior across both residential and commercial assets.

Although the central bank initiated 25-basis-point cuts in the latter half of the preceding year, the prior era of sustained high rates had already established structural blockages. This observation is according to data from MMG Real Estate Advisors.

This transmission chain translates a macroeconomic policy stance into localized market effects. To isolate these divergent paths, it is necessary to map the transmission mechanisms across both sectors. The commercial data presents a quantitative picture of maturity deadlines.

Conversely, the residential effects operate primarily through behavioral economics. Homeowners weigh the cost of relinquishing existing low-rate mortgages against the necessity of moving. By tracking the progression from policy event to second-order implication, market participants can better anticipate market shifts.

| Sector | Event | Mechanism | Primary Market Effect | Second-Order Implication |

|---|---|---|---|---|

| Residential | Fed Rate Hold | Elevated mortgage borrowing costs | Homeowners delay selling (rate lock-in), suppressing spring inventory. | Constrained supply supports prices but slows transaction volume. |

| Commercial (CRE) | Fed Rate Hold | Higher refinancing costs & tighter credit | Landlords face challenges refinancing maturing debt. | Asset transfers and bank write-downs increase as loan extensions decline. |

The residential transmission chain relies on this lock-in effect. Homeowners hold onto inventory to preserve low-interest debt secured prior to 2022. This restricts supply and impacts broader geographic mobility.

For prospective homebuyers, this creates a market characterized by low affordability and limited choices. The second-order effect is a reduction in residential transaction volumes, impacting revenue for real estate brokerages, title companies, and mortgage originators.

In the commercial real estate sector, the transmission mechanism manifests as refinancing challenges. Hundreds of billions of dollars in commercial debt must be refinanced at higher rates. This reduces legacy equity for landlords who cannot cover the new debt service costs. Consequently, institutional capital is increasingly pivoting away from the low-velocity residential sector and toward the commercial sector, where asset clearing is accelerating.

Indicators of Market Transition

The commercial real estate market is transitioning from a period of deferred action into a phase of resolution. Data points from recent quarters indicate that the banking sector’s pandemic-era leniency is concluding, leading to increased asset clearing.

The Decline of Loan Extensions The practice of lenders temporarily modifying loan terms to avoid realizing losses is declining. According to First American, commercial real estate loan extensions falling into the next year decreased from $384 billion (2024 into 2025) to $200 billion (2025 into 2026).

First American data also shows that, measured as a share of expected maturities, these extensions dropped from 41 percent to 21 percent over the same period. This reduction in forbearance indicates that banks and institutional lenders are less inclined to hold impaired loans.

Regulatory pressure and improved clarity on terminal asset values are prompting lenders to act. For U.S. market participants, this signals a phase where borrowers face a choice: inject fresh equity to adjust the capital stack, or transfer the assets to the lender.

The Multifamily Sector and REO Dispositions The decrease in lender leniency is translating into increased financial pressure, particularly within the multifamily sector. Having utilized a significant share of floating-rate bridge debt during peak valuation years, multifamily syndicators are now navigating adjusting capital stacks.

According to MMG Real Estate Advisors, rolling 12-month troubled multifamily volume increased from approximately $1.1 billion in early 2020 to $13.8 billion in recent reporting. Furthermore, MMG Real Estate Advisors notes that multifamily properties accounted for $22.8 billion of the total $126.6 billion in distressed CRE volume recorded in recent quarters.

This financial pressure is moving toward actual market clearing. Multifamily Real Estate Owned (REO) dispositions more than doubled from $1.2 billion in January 2024 to $2.7 billion in recent reporting, according to MMG Real Estate Advisors.

This transition from delinquency to REO disposition implies that regional banks are choosing to realize balance sheet adjustments rather than carrying non-performing loans indefinitely. It also indicates a reduction in limited partner (LP) equity, as syndicators prioritize senior debt or return properties to lenders, establishing new valuation floors for buyers.

Data Discrepancies in Market Reporting While the trajectory of the market is clear, the exact magnitude of the refinancing volume remains uncertain due to conflicting industry reporting. Market participants face a discrepancy regarding the total volume of commercial real estate loans maturing in 2026.

First American cites Mortgage Bankers Association (MBA) estimates of $875 billion in 2026 maturities. Meanwhile, Reuters places the figure at nearly $936 billion. However, broader market estimates from MMG Real Estate Advisors project that over $1.5 trillionand potentially up to $1.8 trillionin CRE loans could reach maturity by the end of 2026.

This potential data gap of nearly $1 trillion highlights opacity in the market. It likely stems from untracked shadow banking, private credit, and mezzanine debt that traditional institutional reporting may not capture. Investors should approach aggregate maturity forecasts carefully. If the true liquidity requirement for 2026 leans toward the $1.8 trillion mark, it could strain the capacity of traditional lending channels and impact asset sale pricing.

Navigating the 2026 Maturity Wall: Scenarios and Uncertainty

The commercial real estate debt market is entering a transition phase. Depending on the interplay between macroeconomic policy and institutional liquidity, the resolution of the 2026 maturities will likely follow one of three paths.

The Base Case: Functional Price Discovery The base case scenario points toward a gradual resolution of market conditions, underpinned by a rebound in commercial mortgage originations. According to the MBA, origination volume is forecast to increase from approximately $634 billion in 2025 to $806 billion in 2026.

This recovery is supported by recent Federal Reserve Senior Loan Officer Opinion Survey data, which indicated an easing in bank CRE lending standards. In this scenario, the market transitions from a slow period to active price discovery. Assets are sold, write-downs are absorbed by capitalized banks, and fresh equity steps in at adjusted valuations. Simultaneously, the residential market experiences a stabilizing inventory recovery as consumers adapt to the new interest rate environment.

The Upside Scenario: Accelerated Rate Relief In an upside scenario, early interest rate relief acts as a catalyst for both CRE refinancing and broader housing supply. If macroeconomic conditions permit the Federal Reserve to accelerate rate cuts, the cost of capital will drop sufficiently to bridge the gap between current valuations and maturing debt obligations.

This dynamic would support the MBA’s projected $806 billion in originations and could push volumes higher as sidelined capital deploys. Furthermore, lower mortgage rates would alleviate the lock-in effect for homeowners, unlocking residential inventory and stimulating transaction volumes. Market participants positioned in bridge lending or preferred equity would see accelerated paydowns and improved portfolio health.

The Downside Scenario: Continued Market Pressure The downside scenario hinges on persistent inflation forcing prolonged high interest rates, compounding the risks of upcoming maturities. With First American reporting lenders pulling back on extensions to 21 percent, borrowers facing maturity without loan modifications would face increased default risk.

If rates remain elevated, the projected $806 billion origination rebound may fail to materialize. This environment could lead to commercial mortgage-backed securities (CMBS) defaults, prompting liquidations at discounted prices. This effect could tighten lending standards further, restricting credit and stalling anticipated recovery in residential inventory.

The probability of these scenarios is influenced by discrepancies in foundational market data. The table below outlines the primary uncertainties that will dictate the market’s trajectory.

| Key Uncertainty | Conflicting Data / Unknown Variable | Market Implication |

|---|---|---|

| 2026 Maturity Volume | Estimates range from $875 billion (MBA) to $936 billion (Reuters) to over $1.5 trillion. | A higher actual volume increases the risk of defaults if origination capital falls short. |

| Rate Cut Timing | Ambiguity surrounds the exact timing of preceding Fed rate cuts. | Delayed rate relief limits refinancing viability and prolongs the residential inventory slowdown. |

| Extension Viability | Extensions dropped to 21% of maturities, but lender capacity to absorb losses remains untested. | If banks cannot absorb write-downs, forced liquidations may suppress asset valuations across the sector. |

What to Watch Next: Leading Indicators of Market Direction

To navigate these crosscurrents, market participants must look beyond aggregate macroeconomic forecasts and monitor a specific checklist of concrete triggers. These indicators will dictate whether the market tracks toward the base, upside, or downside projections.

- Regional Bank Earnings and Loan-Loss Reserves: Because aggregate maturity data varies, investors should monitor regional bank earnings reports for provisioning increases. An increase in loan-loss reserves among mid-sized lenders will serve as a leading indicator that downside risks are materializing and that higher maturity estimates may be accurate.

- Monthly CMBS Delinquency Rates: Track default trends within the commercial mortgage-backed securities market. An upward trend here will indicate that borrowers are facing challenges securing capital, signaling potential liquidations.

- Pace of New Commercial Mortgage Originations: Monitor origination volumes against the MBA’s $806 billion target for 2026. If origination volumes consistently trend upward alongside the easing lending standards noted in recent Federal Reserve survey data, it will support an upside scenario.

- Spring Residential Listing Volumes: Watch for shifts in the residential lock-in effect. An orderly increase in spring listing volumes would signal a transition toward a stabilized base case, indicating that consumers are adapting to the new rate environment.

- Multifamily REO Disposition Rates: As multifamily loan maturities jump 56 percent to roughly $162.1 billion in 2026, according to MMG Real Estate Advisors, the rate at which banks clear REO inventory will be a testing ground for institutional liquidity. Steady disposition clearing suggests the market is finding a functional floor.

Conclusion

The current Fed Rate Hold acts as a catalyst for a structural shift in the real estate market. By maintaining elevated capital costs, the central bank has highlighted a divergence between a slowed residential market and a transitioning commercial sector.

The evidence indicates a decline in loan extensions and an increase in multifamily REO dispositions. This data outlines a clear strategic environment. The reduction of legacy equity in the commercial sectordriven by maturing debt and higher refinancing ratesis establishing adjusted valuation floors.

While this creates near-term challenges for over-leveraged sponsors and regional banks, it simultaneously clears non-performing assets from the system. For well-capitalized investors, the resolution of these maturities is creating entry points to acquire institutional-grade assets at corrected prices. Ultimately, the market is moving from a state of deferred action into a phase of price discovery.

Disclaimer: This analysis is for informational purposes only and does not constitute investment, financial, real estate, or legal advice. Always consult a licensed financial advisor before making investment decisions.

FAQ

How does the Fed rate hold directly affect spring housing inventory? The Fed rate hold keeps mortgage borrowing costs elevated, which solidifies the “lock-in effect.” Homeowners who secured low fixed-rate mortgages prior to 2022 often delay selling to avoid taking on new debt at higher market rates. This retention of existing homes suppresses spring inventory, keeping supply constrained and slowing transaction volume.

Why is 2026 considered a critical transition for commercial real estate debt? 2026 represents a period where a high volume of short-term commercial loans will mature. Estimates range from $875 billion to over $1.5 trillion in maturing debt. Because these loans were largely underwritten during a low-interest-rate environment, borrowers now face higher refinancing costs, leading to increased default risks, equity reductions, and asset sales.

What does the decline of loan extensions mean for multifamily property investors? The decline of loan extensionshighlighted by extensions dropping from 41 percent to 21 percent of expected maturitiesindicates lenders are less willing to delay loss recognition. For multifamily investors, this prompts a resolution phase. Over-leveraged syndicators may see reduced legacy equity as properties are transferred to lenders, evidenced by rising REO dispositions. Meanwhile, well-capitalized investors may gain opportunities to purchase these assets at newly adjusted valuations.