Fed Rate Hold: Navigating Earnings and Multiple Compression

The Fed Rate Hold: Navigating Market Bifurcation and Multiple Compression

The Federal Reserve’s recent decision to maintain its benchmark interest rates is not merely a temporary pause in an otherwise accommodative cycle. Instead, this Fed Rate Hold represents a structural anchor for the U.S. economy, fundamentally altering the macroeconomic landscape for the foreseeable future. This cautious, restrictive stance acknowledges a reality: sticky, persistent inflation is no longer a transitory anomaly, but an entrenched feature of the current economic environment.

For market participants, the confirmation of this “higher for longer” regime dictates an immediate shift in valuation models. Investors can no longer rely on the assumption of an imminent return to zero-bound interest rate policies, meaning the cost of capital will remain an enduring hurdle. The collision of these persistent price pressures with a cooling economic engine sets the stage for a bifurcated market, where robust fundamental earnings are strictly required to justify current equity multiples.

The Transmission Chain: From Policy Hold to Multiple Compression

The foundation of the current valuation environment rests on persistent inflation, which effectively anchors the central bank into a prolonged rate hold. For market participants, this sticky inflation data essentially removes the prospect of imminent rate cuts. Consequently, the risk-free ratetypically represented by U.S. Treasury yieldsremains elevated. This establishes a mechanical transmission chain that directly alters how equities are priced across the broader market.

The transmission mechanism from a restrictive policy stance to equity valuations operates mechanically through the discount rate applied to future cash flows. When the risk-free rate stays high, the weighted average cost of capital (WACC) increases across the corporate spectrum. This forces analysts and institutional investors to apply a heavier discount to corporate earnings expected years down the line.

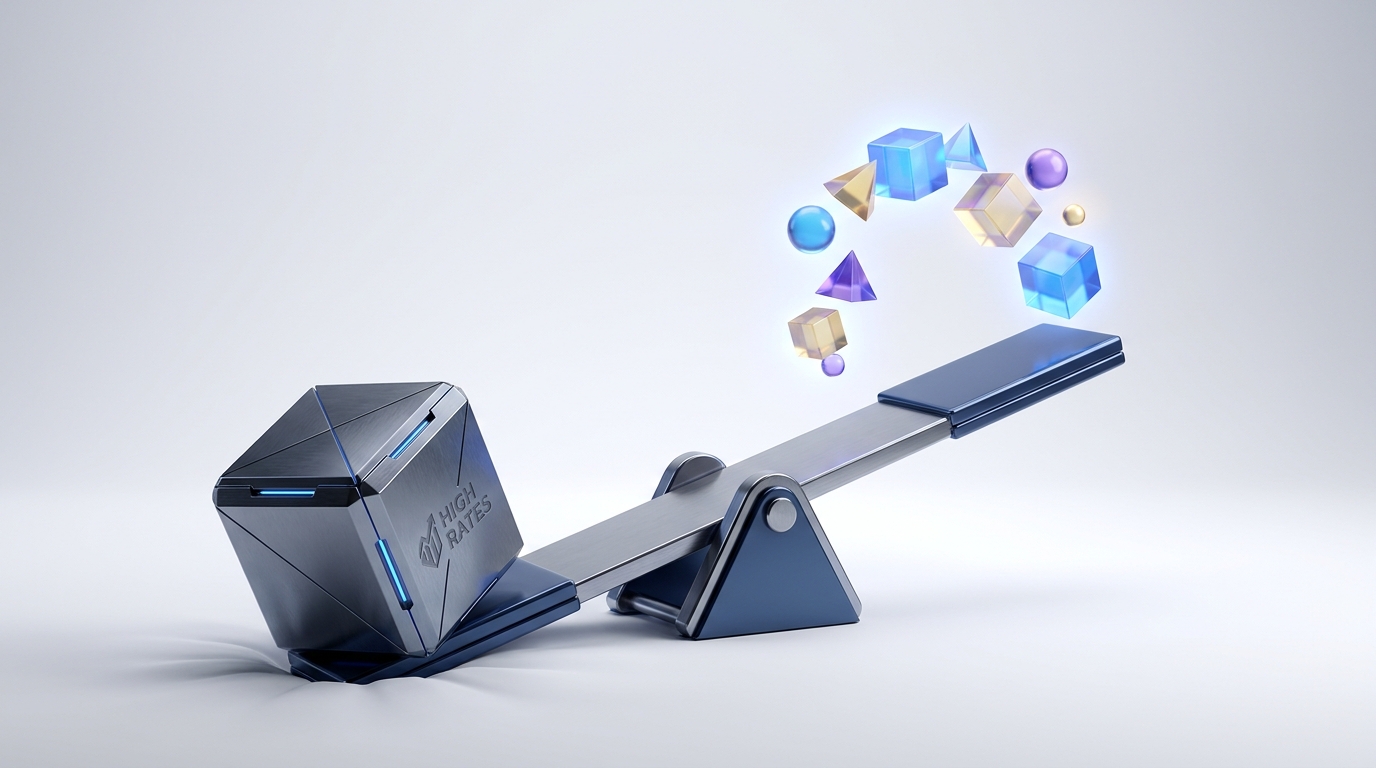

(Visual concept: Imagine a seesaw where one side holds the risk-free interest rate and the other holds growth stock multiples. As the central bank pins interest rates higher, the valuation multiple side of the seesaw is mechanically forced down by the weight of the discount rate.)

This dynamic disproportionately penalizes long-duration growth equities, particularly within the technology sector. The premium valuations of these companies depend heavily on distant profitability rather than immediate, near-term dividend payouts. Ultimately, even if a technology company’s operational trajectory remains intact and its product pipeline is strong, the mathematical reality of a higher discount rate compresses the price-to-earnings multiple investors are willing to pay today.

Yet, a tension exists beneath the surface of this multiple compression, driven by robust underlying corporate fundamentals. Despite the overarching economic headwinds, consensus earnings estimates for the S&P 500 have experienced upward revisions, with particular strength concentrated in the Information Technology sector, according to RBC Wealth Management.

This creates a tug-of-war for tech valuations. The denominator (earnings) is expanding, while the market’s willingness to pay a premium (the multiple) is facing downward pressure from the Federal Reserve’s stance. The fact that the S&P 500 reached a new all-time high prior to mid-April suggests that, for now, earnings growth is overpowering the gravitational pull of higher discount rates, as noted by RBC Wealth Management. However, this dynamic leaves the market vulnerable. The valuation cushion previously provided by expanding multiples has effectively been removed, leaving zero margin for error if future earnings miss expectations.

High-Signal Evidence: The Collision of Inflation and Deceleration

The necessity of this prolonged restrictive policy is underscored by the resurgence of price pressures, heavily driven by volatile commodity markets. The highest-signal data points from recent reports reveal an economy caught between a loss of growth momentum and an erosion of consumer purchasing power.

Numeric Context: The Inflation Anchor

- Metric: Cumulative U.S. Consumer Price Increase

- Timeframe: Since January 2020

- Increase: Exceeds 27%

- Market Implication: Over a quarter of consumer purchasing power has evaporated since 2020. This establishes a permanently higher baseline for nominal prices, restricting the central bank’s ability to ease monetary policy without risking a secondary inflationary spiral. Data sourced from RBC Wealth Management.

By March, the U.S. Consumer Price Index (CPI) accelerated to 3.3 percent. This headline figure was predominantly driven by a 21.2 percent month-over-month increase in gasoline prices, according to RBC Wealth Management. This inflationary spike coincided with physical Brent crude oil peaking at $144 per barrel in early April. While geopolitical optimism regarding a Middle East ceasefire subsequently helped prices retreat to approximately $116 per barrel, near-term inflation expectations were already impacted, per RBC Wealth Management.

The second-order effect of this energy volatility acts as a regressive tax on U.S. consumers. It threatens discretionary spending while simultaneously keeping headline inflation above the central bank’s target. Investors must recognize that as long as commodity markets remain susceptible to geopolitical shocks, monetary policymakers’ options are limited, effectively capping any potential for near-term easing.

Beneath the surface of elevated inflation, high-signal economic data reveals a clear trajectory of decelerating output. While U.S. GDP growth registered at 2.1 percent for the previous full year, the recent trajectory reveals a loss of momentum, according to RBC Wealth Management.

The Bureau of Economic Analysis revised Q4 GDP growth downward in April to 0.5 percent. This is a fundamental contraction from the initial 1.4 percent reading reported just two months prior, RBC Wealth Management notes. A downward revision of this magnitude90 basis pointshighlights a vulnerability in the broader economy as the lagging effects of higher costs and higher borrowing rates materialize on corporate and consumer balance sheets.

| Metric | Timeframe | Rate | Economic Implication |

|---|---|---|---|

| Annual GDP Growth | Previous Full Year | 2.1% | Baseline economic expansion |

| Q4 GDP Growth (Initial) | Q4 (February print) | 1.4% | Emerging deceleration |

| Q4 GDP Growth (Revised) | Q4 (April print) | 0.5% | Loss of momentum |

| Consumer Price Index | March | 3.3% | Persistent, sticky inflation |

Reflecting this broader slowdown, RBC Economics has cut its GDP growth forecast to 1.8 percent, which sits below the consensus estimate of 2.2 percent. This divergence between slowing economic output and stubborn inflation raises the possibility of stagflation. In such an environment, corporate revenue growth becomes increasingly difficult to achieve organically, forcing companies to rely on margin preservation and cost-cutting to maintain profitability.

Despite these macroeconomic headwinds, market participants must distinguish between a cyclical slowdown and a recession. Evidence supporting a broad-based economic contraction remains thin when cross-referenced with actual corporate performance. The apparent disconnect between a 0.5 percent GDP run-rate and the S&P 500 reaching all-time highs is largely driven by concentrated corporate earnings strength, rather than broad economic health.

Capital Allocation: Navigating a Bifurcated Market

The persistence of inflation and decelerating economic growth have firmly entrenched the current interest rate regime, fundamentally altering capital allocation strategies. This combination of sticky inflation and tepid growth forces market participants to reconsider their exposure to long-duration assets. As a second-order effect, investor preference is actively shifting toward sectors that demonstrate immediate cash flow generation, robust pricing power, and inelastic demand.

The Financials sector is emerging as a primary beneficiary of this sustained high-rate environment, offering a defensive yet yield-generating anchor for portfolios. Early indicators from the Q1 earnings reporting season show a positive start for financial institutions, signaling their ability to navigate current economic headwinds, according to RBC Wealth Management.

In a prolonged period of elevated rates, banks and financial services often capitalize on expanded net interest margins, provided that credit quality does not deteriorate. This strong initial earnings performance suggests that the sector is successfully managing default risks while maximizing interest income. For U.S. investors, allocating capital to Financials provides a structural hedge against persistent inflation that continues to erode real returns in other, more speculative segments of the market.

Beyond the financial sector, capital expenditures are undergoing a structural shift as businesses adapt to the maturing economic cycle. Market analysts at Seeking Alpha note an ongoing global industrial rebound and a distinct broadening of capital expenditures outside of the technology sector heading into Q2.

While the Information Technology sector continues to benefit from upward consensus earnings revisions, the expansion of investment into industrial sectors reveals a broader corporate focus on operational efficiency, as highlighted by RBC Wealth Management. Companies in traditional industries are likely reinvesting to harden their supply chains and offset higher input costs through automation and upgraded infrastructure. This rotational dynamic presents opportunities for investors to capture value in cyclical industrial stocks that have previously been overshadowed by technology megacaps. This reliance on mega-cap technology performance masks underlying vulnerabilities in smaller, more credit-sensitive segments of the market.

Valuation Scenarios: Pricing in Uncertainty

The intersection of persistent inflation and decelerating economic growth presents a complex valuation environment for U.S. equities. The divergence between sticky inflation (3.3 percent CPI) and slowing output (0.5 percent Q4 GDP) suggests that monetary policy will likely maintain a restrictive stance longer than markets initially anticipated. This dynamic necessitates a rigorous scenario-based approach to equity valuation, as traditional macroeconomic models struggle to price in the crosscurrents of resilient corporate earnings and geopolitical volatility.

To clearly delineate the uncertainty and risk facing market participants, the following scenarios outline the potential paths for equity valuations under prolonged restrictive policy.

| Scenario | Macroeconomic Driver | Market Catalyst | Implication for U.S. Investors |

|---|---|---|---|

| Base Case: Soft Landing | GDP stabilizes near 1.8% - 2.1%; inflation moderates slowly. | Sector rotation to industrials/financials absorbs tech multiple compression. | Shift allocations toward cyclical sectors for valuation support and broad market exposure. |

| Upside: Tech Dominance | Productivity gains offset high interest rates; energy prices stabilize. | IT sector earnings revisions outpace the drag of higher discount rates. | Overweight growth equities; structural tech advantages drive broader market gains. |

| Downside: Stagflation | GDP decelerates below 1.4%; CPI remains sticky above 3.0%. | Energy shocks compress margins; rates remain restrictively high. | Defensive positioning required; traditional portfolios face simultaneous asset drawdowns. |

The Base Case: A Soft Landing and Sector Rotation In the base case scenario, the U.S. economy achieves a soft landing characterized by a healthy sector rotation that absorbs any multiple compression in high-valuation technology stocks. Evidence of this rotation is already emerging, with the Financials sector posting a strong start to the Q1 earnings season, according to RBC Wealth Management. Furthermore, the broadening of capital expenditures beyond the technology sector heading into the second quarter implies that capital is migrating toward cyclical and value-oriented sectors, as noted by Seeking Alpha. These sectors historically offer better downside protection when discount rates remain elevated. Market participants can position for a more durable, broader-based rally where industrials and financials provide the earnings growth necessary to sustain index levels even if macroeconomic headwinds persist.

The Upside Scenario: Technological Dominance Overcomes Rates The upside scenario hinges on the Information Technology sector’s ability to generate earnings growth that fundamentally outpaces the valuation drag of higher discount rates. Despite the unfolding Middle East crisis and physical Brent crude prices temporarily spiking to $144 per barrel, consensus earnings estimates for the S&P 500particularly within the IT sectorexperienced upward revisions, per RBC Wealth Management. Analytically, this suggests that the market is pricing in structural productivity gains within the tech sector that are relatively immune to cyclical borrowing costs. If these tech earnings revisions continue to materialize, U.S. equities could experience broader market gains driven by a combination of mega-cap resilience and an expanding economic base.

The Downside Scenario: Stagflation and Margin Compression Conversely, the downside scenario introduces the risk of stagflation, where economic output continues to decelerate while inflation forces interest rates to stay high. The downward revision of Q4 GDP to 0.5 percent and RBC Economics’ lowered GDP growth forecast of 1.8 percent highlight the fragility of the current expansion, according to RBC Wealth Management. If geopolitical tensions reignite energy price shocks and keep the CPI structurally elevated above central bank targets, corporate margins will compress. This stagflationary environment would likely trigger a synchronized contraction in both equity multiples and earnings estimates across all sectors. Investors must recognize that in this downside risk environment, traditional diversification strategies may fail, as both equities and fixed income would suffer simultaneously under the weight of persistent inflation and stalling growth.

What to Watch Next: Triggers and Indicators

As the central bank maintains its current policy stance, market participants face a complex macroeconomic environment that requires vigilance. The tension between a restrictive policy and resilient equity markets will likely define the remainder of the year. To navigate this regime, investors must monitor several high-frequency indicators and upcoming data releases to determine which valuation scenario is unfolding.

1. GDP Revisions and Growth Metrics The trajectory of U.S. economic expansion is showing clear signs of vulnerability, making upcoming growth metrics a critical trigger for asset allocation. Investors must closely watch for any subsequent revisions to the Q4 GDP figure, which the Bureau of Economic Analysis already revised downward from 1.4 percent to 0.5 percent in April, according to RBC Wealth Management. If upcoming data releases validate this deceleration, it will challenge the consensus GDP forecast of 2.2 percent and align reality closer to RBC Economics’ 1.8 percent projection. A confirmed trend of deteriorating growth would likely prompt a rapid market rotation out of cyclical equities.

2. Industrial Capex Deployment The trajectory of Q2 industrial capex deployment will serve as a leading indicator for broader economic health and market breadth. Analysts at Seeking Alpha have noted an ongoing global industrial rebound and a broadening of capital expenditures beyond the Information Technology sector heading into the second quarter. Investors must verify whether this Q2 capex deployment actually materializes. Execution here would indicate that businesses are successfully adapting to higher capital costs by investing in physical productivity rather than retrenching. A failure of this industrial momentum to materialize would leave the recent S&P 500 all-time highs dependent on a narrow cluster of technology stocks.

3. Bank Earnings and Credit Quality The ultimate validation of the “higher for longer” thesis rests on the banking sector’s performance in the coming weeks. The Financials sector has already demonstrated a positive start to the Q1 earnings reporting season, per RBC Wealth Management. Investors need to watch whether this Q1 momentum sustains through the remainder of the reporting period, as banks act as the primary transmission mechanism for monetary policy. Strong forward guidance from financial institutions would confirm that credit demand remains robust and default risks are contained. Conversely, if bank executives begin signaling rising loan-loss provisions or tightening credit standards, it would serve as an early warning that the current rate environment is impacting corporate fundamentals.

Conclusion

The current macroeconomic reality is defined by a friction between resilient corporate earnings and a decelerating broader economy. The central bank’s commitment to a Fed Rate Hold fundamentally dictates that the era of speculative, liquidity-driven equity rallies has ended. With cumulative consumer prices up over 27 percent since 2020 and GDP growth slowing to a 0.5 percent run-rate, the margin for macroeconomic error has effectively vanished.

For investors, the evidence points to a necessary shift in strategy. The mechanical pressure of higher discount rates will continue to penalize long-duration assets that lack immediate cash flow. However, the upward revisions in technology earnings and the broadening of industrial capital expenditures prove that opportunities remain for companies demonstrating inelastic pricing power and strong balance sheets. Ultimately, navigating this environment requires prioritizing disciplined capital allocation and margin preservation. Market participants must accept that the cost of capital will remain an enduring hurdle, and only those equities backed by tangible, near-term cash generation will successfully defend their multiples against the gravitational pull of restrictive monetary policy.

Disclaimer: This analysis is for informational purposes only and does not constitute investment, financial, real estate, or legal advice. Always consult a licensed financial advisor before making investment decisions.

FAQ

How does a Fed rate hold negatively affect growth and tech stock valuations? A rate hold keeps the risk-free interest rate elevated, which mechanically increases the weighted average cost of capital (WACC) for the broader market. This forces analysts to apply a heavier discount rate to future corporate earnings. Because growth and tech stocks derive much of their valuation premium from expected profitability years down the line, this higher discount rate compresses the price-to-earnings multiple investors are willing to pay today.

Which equity sectors historically perform best during a ‘higher for longer’ interest rate regime? Sectors that demonstrate immediate cash flow generation and robust pricing power tend to outperform. The Financials sector often benefits, as banks can capitalize on expanded net interest margins provided credit quality remains stable. Additionally, cyclical Industrials can perform well as companies broaden capital expenditures to harden supply chains and improve operational efficiency to offset higher input costs.

Will the broadening of global industrial capex offset the slowdown in U.S. GDP growth? It depends on the execution of these investments and the broader macroeconomic environment. In a base case “soft landing” scenario, a broadening of industrial capex can provide the necessary earnings growth to sustain market levels and absorb multiple compression in the tech sector. However, if persistent inflation and energy shocks lead to a stagflationary downside scenario, industrial momentum may fail to materialize, leaving the broader market vulnerable to the underlying GDP deceleration.