What the Fannie/Freddie MBS Proposal Means for Housing

How the New Fannie/Freddie MBS Proposal is Rewiring U.S. Markets

The financial markets are currently digesting a structural shift that fundamentally alters the trajectory of U.S. monetary policy and asset pricing. At the center of this transformation is President Donald Trump’s recent executive directive ordering government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac to expand their purchases of mortgage-backed securities (MBS), according to ca.finance.yahoo.com. For institutional and retail investors alike, this Fannie/Freddie MBS Proposal functions as a form of quantitative easing (QE). It is a policy shift that matters immediately because it introduces targeted liquidity into the financial system, acting as a direct counterbalance to the Federal Reserve’s prolonged interest rate pause.

To understand the timing of this executive intervention, one must look at the slowdown in the U.S. housing sector. While the broader macroeconomic environment has remained resilient, the real estate market has been constrained by elevated borrowing costs. High interest rates have kept prospective buyers sidelined, creating a localized economic slowdown within the housing supply chain. The administration’s mandate is a targeted intervention designed to break this deadlock. By compressing mortgage rates, policymakers are attempting to stimulate housing demand before the stall triggers a broader economic contraction. Consequently, investors must now price in a complex new environment where executive directives are deployed to offset restrictive central bank policies, fundamentally changing the risk-reward calculus across fixed-income and equity markets.

The Transmission Chain: From Executive Directive to Market Impact

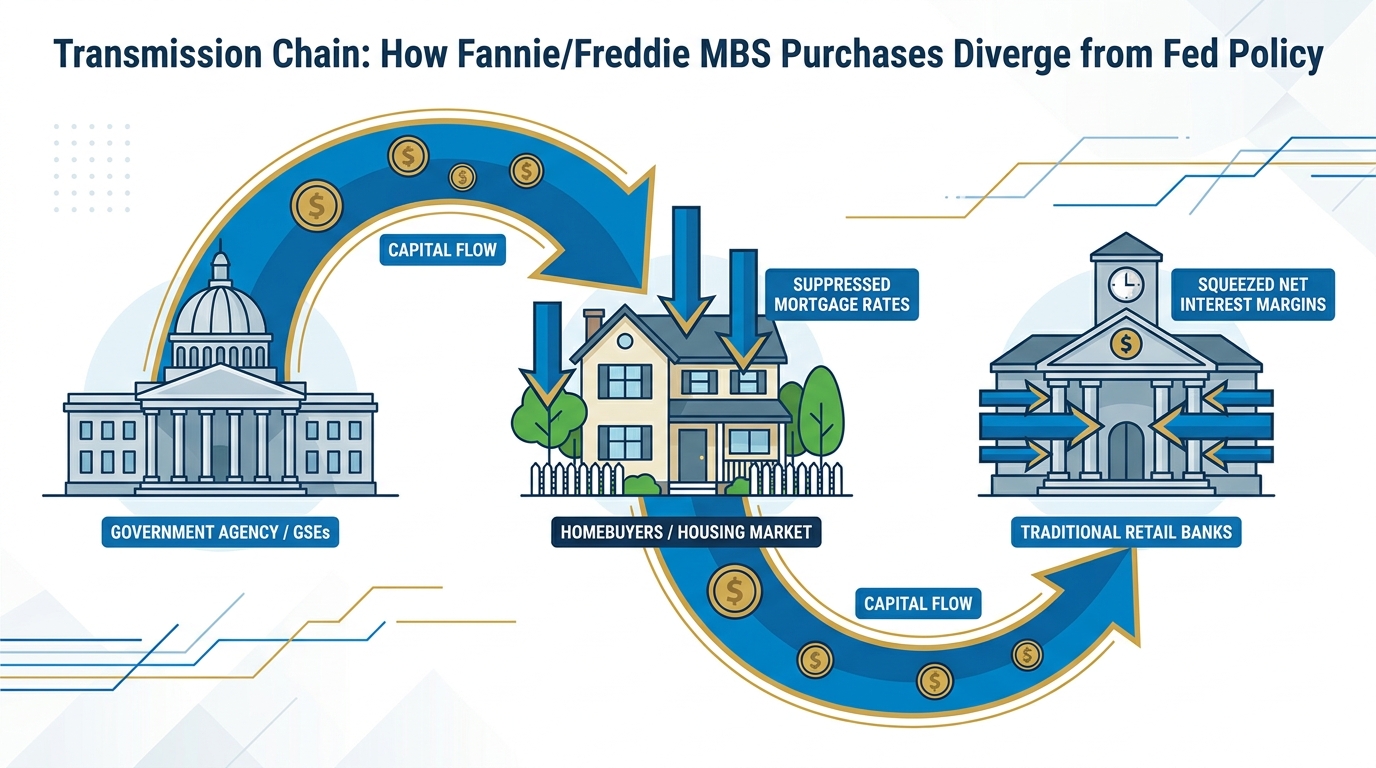

The catalyst for the current divergence in mortgage market dynamics begins at the executive level but transmits rapidly through the plumbing of the fixed-income markets. This transmission chain is a specific, sequential flow of capital that bypasses traditional Federal Reserve monetary policy channels. By utilizing the GSEs as direct instruments to influence market pricing, the administration has installed non-economic buyers as a dominant marginal force in the mortgage debt market.

The sequence begins with the government directive, which triggers MBS absorption by Fannie Mae and Freddie Mac. The immediate result of this mandate has been a rapid balance sheet expansion. Data from Investing.com reveals that the combined portfolios of Fannie Mae and Freddie Mac increased by 25% over a five-month period. To put this into perspective, HousingWire reports that Fannie Mae’s retained mortgage portfolio alone surged from $89.3 billion in 2023 to $123.4 billion by the end of 2024.

As these government-backed entities absorb these mortgages onto their own balance sheets, they systematically drain the available supply of fixed-income products from the open market, as noted by Investing.com. In any market, when a dominant buyer reduces supply, prices rise and yields fall. This supply-demand imbalance naturally pushes yields on both MBS and U.S. Treasuries lower. More importantly, it compresses MBS spreads toward U.S. Treasury yields, according to Investing.com. The traditional risk premium associated with mortgage prepayment and duration risk is being suppressed by sovereign-level intervention.

This engineered yield suppression is a targeted attempt to clear the housing market’s affordability logjam. By pushing mortgage rates down, the policy directly provides structural tailwinds for mortgage originators and homebuilders. It offers a critical lifeline to a sector constrained by buyers waiting on the sidelines for rate relief. However, this transmission chain generates second-order consequences for the broader financial sector. As the GSEs crowd out private buyers and compress MBS spreads, the traditional risk-reward models used by fixed-income investors are upended. Market participants are increasingly adopting the mantra “Don’t fight the GSEs,” signaling that quantitative models must now heavily weight this persistent, policy-driven bid reported by Investing.com.

High-Signal Evidence: The Macro Divergence

To fully contextualize the necessity and scale of this GSE intervention, analysts must examine the dichotomy between the general economy and the housing market. The economic landscape presents a divergence between broad macroeconomic resilience and localized weakness in the real estate sector. This divergence is the fundamental justification for the administration’s intervention.

On one side of the ledger, historical data illustrates how the broader economy has demonstrated resilience. In January 2023, the U.S. labor market showed unexpected strength as employers added 517,000 workers, driving the unemployment rate down to 3.4%, according to Chandler Asset Management. Concurrently, one-year consumer inflation expectations proved sticky, moving up to 4.2% in February 2023 from 3.9% the prior month, as noted by Chandler Asset Management. This combination of a strong labor market and entrenched inflation expectations effectively restricts traditional monetary easing. If the Federal Reserve were to enact broad rate cuts in this environment, they would risk reigniting inflationary pressures.

On the other side of the ledger, the housing market has shown recessionary signals. Builder sentiment reflects a broken capital cycle. The National Association of Home Builders (NAHB)/Wells Fargo Housing Market index has remained below the 50 break-even point for 23 consecutive months, recently edging up only slightly to 38, according to ca.finance.yahoo.com.

The following table illustrates the high-signal metrics driving this policy divergence, contrasting historical aggregate resilience against sector-specific decay:

| Metric Category | Key Indicator | Latest Data Point | Market Implication |

|---|---|---|---|

| Macro Resilience | January 2023 Jobs Added | 517,000 | Indicates robust aggregate demand |

| Macro Resilience | Unemployment Rate (Early 2023) | 3.4% | Suggests a persistently tight labor market |

| Macro Resilience | 1-Year Inflation Expectations | 4.2% | Constrains broad monetary easing policies |

| Housing Weakness | NAHB Housing Market Index | 38 | Signals builder pessimism and contraction |

The depth of this housing weakness is further evidenced by the defensive posture of residential developers. Facing elevated costs for land, labor, and construction, 37% of homebuilders have resorted to outright price cuts to stimulate demand, as reported by ca.finance.yahoo.com. Furthermore, nearly two-thirds (64%) of builders are relying on margin-eroding sales incentives to maintain buyer interest, according to ca.finance.yahoo.com.

For market participants, these metrics indicate that the housing sector is undergoing a margin compression cycle. Builders are sacrificing profitability just to clear inventory, signaling that organic market clearing without external support remains unlikely. The proposed $200 billion mandate for Fannie Mae and Freddie Mac to purchase agency MBS represents a demand shock designed to bypass the Fed’s restrictive posture. This targeted approach allows policymakers to provide relief to prospective homebuyers and builders without altering the broader, restrictive monetary stance required to combat 4.2% inflation expectations.

Market Scenarios: Base Case, Upside, and Downside Risks

The expansion of GSE balance sheets is creating a bifurcated equity market environment. As the prevailing market adage evolves to “Don’t fight the GSEs,” fixed-income investors face the prospect of structurally suppressed yields, as observed by Investing.com. This dynamic forces capital into higher-yielding equities and corporate credit, providing artificial support to stock indices, but the impacts will be felt unevenly across sectors.

The Base Case: Homebuilder Relief vs. Regional Bank Pain In the base case scenario, homebuilders will rally as suppressed mortgage rates stimulate buyer traffic and clear the affordability logjam. However, this same spread compression forms the basis for a bearish outlook on regional banks. Regional banks rely heavily on the spread between short-term deposit costs and the yields generated by long-term assets, with MBS forming a core component of their investment portfolios.

As the GSEs crowd out private buyers and compress MBS spreads, regional banks are forced to reinvest maturing assets into lower-yielding securities. This structurally impairs their core profitability, resulting in net interest margin (NIM) compression. The financial toll of this engineered market dynamic is already visible; Fannie Mae’s own fourth-quarter 2024 earnings report noted that the majority of its fair-value losses were driven by this exact compression in interest rate spreads, according to HousingWire. If a well-capitalized entity like Fannie Mae is realizing fair-value impacts from compressed spreads, regional banks with less sophisticated hedging operations will likely suffer more acute NIM degradation. While lower yields may marginally reduce the risk of loan defaults by easing borrower burdens, investors holding financial sector equities must weigh this benefit against the detrimental impact of engineered NIM compression.

The Upside Scenario: Operational Efficiencies Expanding Margins In an upside scenario, internal operational efficiencies within the GSEs could amplify margins across the broader mortgage origination ecosystem. Fannie Mae successfully reduced its administrative expenses in 2024 for the first time in four years, cutting its workforce by roughly 1,200 employees and trimming noninterest expenses by $141 million, as reported by HousingWire. This disciplined expense management helped secure a $14.4 billion net profit for the year and resulted in a $109 billion net worth, according to HousingWire.

This signals a maturation in operations that could streamline core processes and technology infrastructure. For U.S. investors, this implies that non-bank mortgage originators and servicers interacting directly with Fannie Mae could experience reduced friction and lower transaction costs. If these operational efficiencies are passed down the supply chain, originator margins could expand even in a lower-yield environment, providing a distinct upside catalyst for the broader real estate finance sector.

The Downside Scenario: Macroeconomic Gravity and Timeline Uncertainty The primary downside scenario centers on macroeconomic risks, specifically a re-acceleration of inflation that could derail the GSE-driven spread compression. Homebuyer activity continues to be suppressed by elevated land, labor, and construction costs, alongside significant down-payment hurdles, according to ca.finance.yahoo.com. Furthermore, geopolitical tensions, particularly the conflict with Iran and fluctuating oil prices, introduce exogenous inflationary pressures, as noted by ca.finance.yahoo.com.

If these external shocks drive inflation higher, the Federal Reserve may be forced to resume rate hikes, which would negate the artificial support for MBS yields. Higher benchmark rates would immediately increase borrowing costs, freezing the anticipated homebuilder rally and stalling the broader economic stabilization process. Additionally, evidence regarding the exact deployment timeline of broader liquidity injectionssuch as the rumored $200 billion market interventionremains thin and uncertain. If macro pressures force the GSEs to halt their portfolio ramp-up prematurely, housing equities will be left vulnerable to a correction.

What to Watch Next: Key Indicators and Triggers

As the Federal Reserve maintains its ongoing rate pause, base interest rates remain anchored, forcing investors to look beneath the surface for yield drivers. In this environment, structural market interventions are beginning to outweigh traditional macroeconomic shifts. Investors must continuously monitor specific indicators to navigate this policy-driven market.

- Agency MBS Spreads vs. U.S. Treasuries: The most immediate metric for fixed-income investors to monitor is the daily tracking of agency MBS spreads relative to U.S. Treasuries. With the GSEs’ combined portfolios already up 25% in five months, according to Investing.com, continued spread compression will confirm that the GSEs are overriding organic market pricing.

- Regional Bank Earnings and NIM Guidance: Upcoming regional bank earnings reports are a critical watchpoint. Investors must pay close attention to management’s forward guidance on Net Interest Margins. If MBS yields fall faster than deposit costs can adjust, regional banks will likely forecast further NIM compression, signaling profitability headwinds.

- The NAHB/Wells Fargo Housing Market Index: The fundamental health of the housing sector hinges on upcoming releases of this index. Having remained below the 50 break-even point for 23 consecutive months, as reported by ca.finance.yahoo.com, a sustained move above 50 would signal a definitive shift from contraction to expansion in homebuilder confidence.

- Builder Sales Incentives: Investors should continuously track the share of builders offering sales incentiveswhich recently dipped slightly to 64% but remains elevated, according to ca.finance.yahoo.comas a real-time proxy for consumer demand elasticity in a high-friction environment.

- Geopolitical and Inflationary Shocks: The trajectory of the housing recovery is complicated by persistent external headwinds. Monitoring geopolitical conflicts involving Iran, fluctuating oil prices, and sticky consumer inflation expectations (historically around 4.2% as noted by Chandler Asset Management) is essential to gauge whether exogenous shocks will overpower the GSE liquidity injection.

Conclusion

The administration’s utilization of Fannie Mae and Freddie Mac to absorb mortgage debt represents a paradigm shift in U.S. financial markets. By bypassing traditional monetary policy channels, the government is engineering a targeted liquidity injection designed to rescue a stalled housing sector while the broader economy remains constrained by sticky inflation and a tight labor market. The analytical takeaway for market participants is clear: the primary driver of mortgage yields has temporarily shifted away from central bank dot plots and toward GSE balance sheet capacity.

This structural intervention creates a bifurcated landscape. It provides an artificial floor for asset prices and offers a lifeline to homebuilders and mortgage originators, but it simultaneously inflicts collateral damage on regional banks through engineered net interest margin compression. Ultimately, the success of the Fannie/Freddie MBS Proposal hinges on a fragile equilibrium. While sovereign-level balance sheet expansion provides a technical bid for mortgage-backed securities, the fundamental recovery of housing equities remains vulnerable to consumer anxiety, entrenched inflation, and exogenous geopolitical shocks that executive directives cannot easily resolve. Investors must now navigate a market where fighting the GSEs is just as perilous as fighting the Fed.

Disclaimer: This analysis is for informational purposes only and does not constitute investment, financial, real estate, or legal advice. Always consult a licensed financial advisor before making investment decisions.

FAQ

How does the Fannie/Freddie MBS proposal act as quantitative easing? The proposal functions as a form of quantitative easing by utilizing government-sponsored enterprises (GSEs) to purchase mortgage-backed securities (MBS) from the open market. This absorption of debt injects targeted liquidity into the financial system and reduces the supply of fixed-income products, which systematically pushes yields lower and compresses MBS spreads without requiring the Federal Reserve to formally cut benchmark interest rates.

Why are regional banks at risk of Net Interest Margin (NIM) compression from this policy? Regional banks rely heavily on the spread between the short-term costs of holding customer deposits and the yields generated by long-term assets, such as MBS. As the GSEs dominate the bond market and compress MBS spreads, regional banks are forced to reinvest their maturing assets into these lower-yielding securities. Because their deposit costs remain high due to the Fed’s rate pause, this dynamic structurally impairs their core lending profitability and compresses their net interest margins.

How will suppressed mortgage yields impact homebuilder and originator stocks? Suppressed mortgage yields provide a direct structural tailwind for homebuilders and mortgage originators. Lower borrowing costs help clear the housing market’s affordability logjam, stimulating buyer traffic for a sector that has seen builder sentiment trapped in contractionary territory for 23 consecutive months. This policy intervention allows builders to potentially reduce their reliance on margin-eroding price cuts and sales incentives, offering a lifeline to their equities.

Why is the administration intervening in the housing market while the Fed pauses rates? The administration is intervening because the U.S. economy is experiencing a localized slowdown in the housing sector despite broader macroeconomic resilience. With a historically tight labor market and sticky inflation expectations, the Federal Reserve is constrained from cutting rates broadly without risking a re-acceleration of inflation. The executive directive allows the administration to bypass this restrictive monetary environment and provide targeted, localized relief specifically to the interest-rate-sensitive real estate sector.